Applying Analytical Frameworks to Personal Wealth Optimization

Turning data thinking into smarter saving, investing, and decision-making

Most people manage money by emotion. We spend when we're happy, save when we're scared, and invest when everyone else won't stop talking about it. It works, sometimes but it isn't a system, and it doesn't scale.

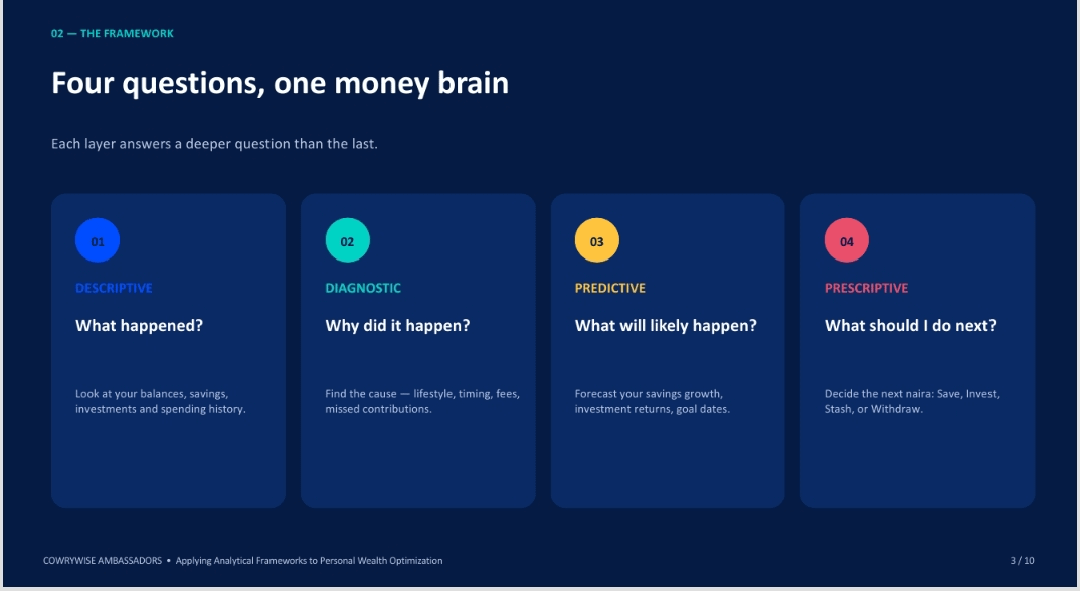

There are four frameworks analysts use to make sense of almost any business question: Descriptive, Diagnostic, Predictive, and Prescriptive analytics. Strip away the jargon, and they're really just four honest questions:

What happened?

Why did it happen?

What's likely to happen next?

What should I do about it?

Here's the part that changed how I think about my own money: those are exactly the right questions to ask about youra, too.

This is the system I walked through in this week's webinar for Lagos State Cowrywise ambassadors and I wanted to put it in writing so you can actually apply it this week

1. Descriptive Analytics: What is actually happening with my money?

Before you can fix anything, you need an honest picture. No optimization, no strategy, no behavior change works until you can describe your current state in plain language.

If you can't describe your money in one sentence, you can't optimize it. Description always comes first.

2. Diagnostic Analytics: Why is my money behaving this way?

Once the picture is clear, ask why. This is where most people stop , they notice a problem ("I never seem to have savings") but never dig into the cause. Diagnostics is the uncomfortable, useful step.

Three questions to run on yourself:

Where is my money sleeping?

Why am I not topping up?

Which fees am I paying repeatedly?

Most underperformance isn't a market problem — it's a behavior problem.

3. Predictive Analytics: What's likely to happen if I keep going?

This is where it gets exciting, because now you're not just looking backward you're projecting forward. Your Invest tab gives you the raw building blocks for a personal forecast.

A few simple moves:

Estimate an annual return. Mutual funds typically run ~10–18%; stocks are more variable.

Project a goal date. If you add a fixed amount every month at a 12% annual return, you can work out almost exactly when you'll hit your target. That's not magic it's arithmetic, and it's available to anyone willing to do it.

Stress-test the plan. What happens if returns drop 30% from your estimate? Does the goal date still hold, or does the plan collapse? Better to know now than to be surprised later.

Use your own history as a baseline.

A forecast is not a promise. It's a steering wheel for the decision you're about to make today.

4. Prescriptive Analytics: What should I actually do next?

This is the step that makes the first three worth doing. With a clear description, an honest diagnosis, and a realistic forecast in hand, every money gets an instruction: Save it, Invest it, Stash it, or Withdraw it. Nothing sits there by default anymore.

Set a standing monthly review. The 1st of every month, re-run all four questions. This isn't a one-time fix; it's a habit.

The takeaway: don't just look at the data let it decide where the next money lands.

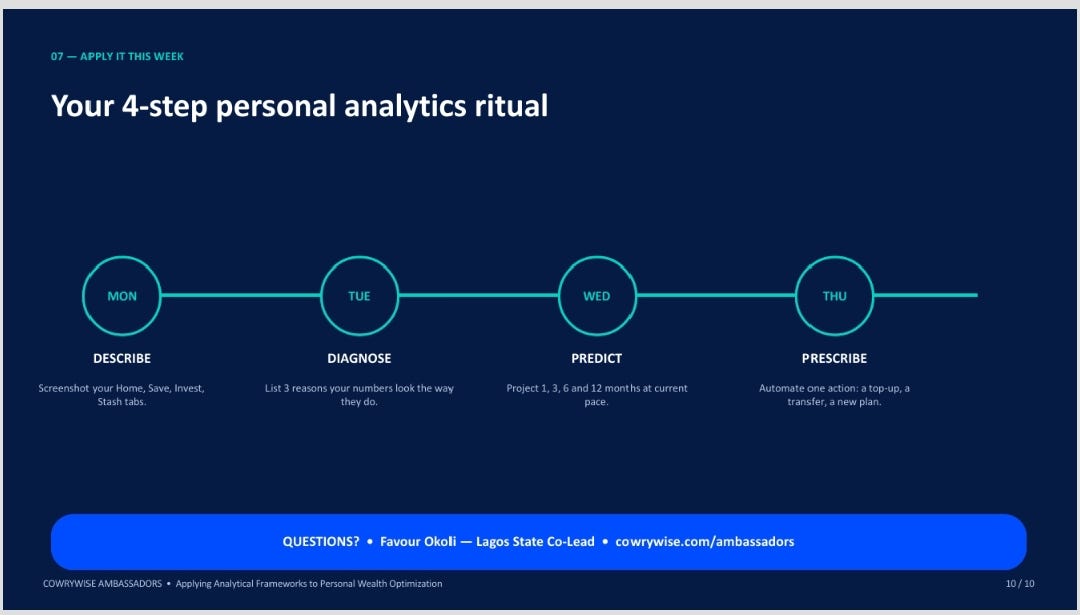

Your 4-Day Personal Analytics Ritual

If you want to put this into practice this week, here's the simplest version:

That's it. Four days, four questions, one decision system you can reuse every single month.

The frameworks data analysts use to solve million-naira business problems work just as well on your own account balance. You don't need a finance degree to use them, you need fifteen honest minutes with your own numbers.

If you found this useful, you can always reach out for the slides . I'm always glad to talk through someone's specific numbers.